2026 Housing Market Outlook

The upcoming year brings continued progress toward normalization while building resilience

The U.S. housing market is expected to shift toward recovery in 2026, transitioning away from the volatility that followed the pandemic. Forecasts point to more typical market conditions: mortgage rates stabilizing near 6%, home prices rising 2%–4% and modest improvements in affordability and the number of homes for sale. Still, significant obstacles, including rising non-mortgage costs, constrained affordability and uneven regional performance, will continue to shape buyer and seller decisions.

The Federal Reserve’s anticipated policy easing should gradually reduce borrowing costs, though volatility will persist. Mortgage rates are expected to stay above 6% throughout 2026, fluctuating between roughly 5.8% and 6.4%. Even a modest decline provides some payment relief compared with 2024–2025.

Falling rates will also spur more refinancing, especially for homeowners who purchased recently. Cotality data shows about 5.2 million loans originated since 2022 at rates of 6% or higher. If rates drop to 6%, roughly 3 million borrowers would qualify for refinancing incentives. This shift could also unlock nearly 2 million homes as refinance-eligible owners reevaluate moving or listing their properties.

Nationwide, home prices are expected to rise about 3% in 2026, with regional growth ranging from 2% to 4%. Adjusted for inflation, prices will remain mostly flat, offering slight affordability gains if wage growth continues near its current 4% pace.

Regional divergence is set to continue. The Northeast and Midwest should see gains of 3%–4% due to limited supply and steady demand. The Sun Belt and West, areas that absorbed much of the pandemic-era migration, will experience slower appreciation, with some markets likely to see stable or slightly declining prices as valuations realign with local incomes and rising ownership costs. Economic fundamentals, rather than migration surges, are expected to drive regional dynamics going forward.

Inventory has risen for 24 consecutive months, helped by an uptick in new construction in certain regions. Yet nationwide supply remains about 15% below pre-pandemic levels and when adjusted for population growth, at historically low levels. Returning to early-2000s norms would require roughly 1.5 million additional existing homes on the market.

Inventory is expected to increase another 5%–10% in 2026, driven largely by life-stage transitions or financial pressures that prompt some owners to sell. However, factors like capital gains tax exposure and lingering affordability challenges continue to hold many homeowners in place.

Investor behavior is shifting as well. After years of high activity, rising holding costs, slower rent growth and weaker short-term rental demand are pushing some investors to sell, particularly in Western and Southern markets, boosting available inventory. Stronger new construction in parts of the South and Southeast is also contributing to improved supply. Even so, structural shortages persist because of zoning hurdles, rising construction costs and ongoing labor constraints. The Midwest and Northeast will likely remain tight, while the South and West see more listings.

Single-family housing starts should remain relatively flat in 2026, though current levels exceed any single year from 2008 to 2019. Builders continue to contend with labor shortages, expensive land and elevated material costs. Incentives, such as mortgage rate buydowns and closing-cost credits, will remain key to maintaining sales, particularly in regions where new homes offer buyers more choices and leverage.

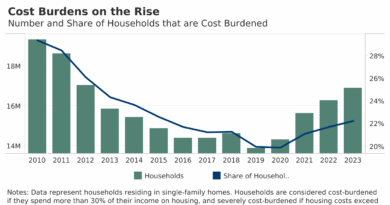

Affordability may improve slightly as price growth moderates and mortgage rates edge down. But non-mortgage ownership costs are putting increasing pressure on households. Insurance, utilities and property taxes, costs typically included in escrow payments, have risen by about 30% on average since 2019. In states such as Florida and Colorado, escrow costs have surged 55%–57%.

Insurance premiums alone have climbed 40%–60% since 2019, now averaging $2,370 annually. They are projected to rise another 8% in 2026, outpacing overall inflation. Property taxes, already up roughly 30% nationwide, are expected to continue climbing as local governments respond to population growth and heightened demand for services. These increases erode the modest affordability gains from slower home price appreciation and lower mortgage rates. At the same time, years of rising rents have made it harder for first-time buyers to save for down payments, further limiting access to homeownership.

The 2026 housing market should show continued stabilization: moderating mortgage rates, modest home price growth, improving inventory and rebounding sales. This marks a shift from the sharp volatility of the past few years toward a more balanced environment. Still, significant challenges remain, especially a shortage of affordable homes and rising non-mortgage costs that strain household budgets. Buyers and sellers navigating this market will need patience and well-informed strategies, as the recovery will be gradual rather than dramatic.

By Dr. Selma Hepp. She is the Chief Economist of Cotality. She may be reached at newsmedia@cotality.com

By Dr. Selma Hepp. She is the Chief Economist of Cotality. She may be reached at newsmedia@cotality.com

This column also appears in the January issue of Builder and Developer, read the print version here.