2026 Housing Playbook for Builders & Developers

After a challenging 2025, the housing market is heading into 2026 with expectations of a moderate year. The real upside looks to return in 2027 but only for firms that pivot. The old cycle playbook won’t work. Here’s what matters most and how to respond.

Mortgage rates are near normal but don’t underwrite for a big drop. The 40-year tailwind of falling rates is over. Mortgage rates today are already close to where the Fed wants them and long-term historical norms point rates remaining in mid-6% territory. Hoping for a dramatic rate decline isn’t a strategy and if rates fall sharply, it’s likely because the economy weakens, which likely hurts housing demand more than lower rates help.

Some of the implications for 2026 are to: assume only modest rate relief in underwriting, focus on margins, mix and velocity, not rate-dependent volume surges and stay nimble so you can scale quickly if rates surprise lower.

Many experts have claimed that the U.S. is undersupplied by anywhere from 3 to 7 million homes. On top of fewer-than-normal homes available to buy or rent, there is certainly evidence of additional pent-up demand for housing, just look at the unusually high numbers of 25–34-year-olds who are doubling up by living with parents or taking roommates, largely due to affordability stress.

But at current prices and rents, today’s net undersupply is around 1.1 million homes and shrinking. Affordability remains challenged, especially for first-time buyers.

The binding constraint is affordability, not raw unit counts and building more expensive “standard” products won’t clear demand. Instead builders should design monthly payment targets first, treat attainable products as a core business, not an edge case and keep plans flexible for smaller footprints and attached formats.

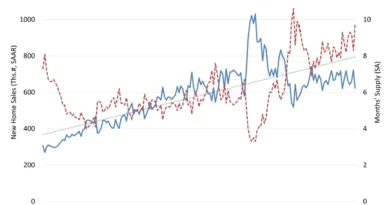

Predicting that starts will stay muted in 2026 for five structural reasons; first is, the U.S. has too many unsold, finished new homes. Today’s inventory of homes is near 2008 levels in aggregate and builders are throttling starts so sales can outpace deliveries and clear finished inventory. Second, land sellers continue to resist price cuts, which means that fewer land deals pencil right now. Third, housing demand has slowed as job growth has decelerated. Fourth, entry-level affordability has collapsed. Despite incomes rising ~26% since 2020, home prices are up ~45%, combined with higher mortgage rates, monthly payments for entry-level buyers are up ~82% in that time. Lastly, the lock-in effect still weighs on the market: about 70% of mortgaged homeowners have a mortgage rate below 5%, which is slowing resale churn.

Although it is not suggested to expect meaningful national growth until land prices and inventory clears. Re-trading land, managing your flows to where sales outpace starts in order to normalize specs and competing harder with resale by providing turnkey value and sharper product is a good approach.

Rental demand is strong, but so is supply. Right now, absorptions and deliveries are roughly a wash, which is why rent growth has been modest. The good news? Multifamily starts are down enough that deliveries should normalize by late 2026, allowing modest rent growth to return, especially in select Midwest markets and near new tech employment.

Moderate rent growth is expected, not a boom, but steadier than for-sale. While build-to-rent remains a long-term winner, even if some submarkets are currently overbuilt.

It is best to pursue build-to-rent where feasibility works, underwrite conservatively for 2026 lease-up, but keep a bullish view for 2027 and beyond and consider buying below replacement cost or high-yield lending until construction pencils more easily.

Households are leapfrogging from expensive cores to nearby value markets. We see examples of this where households priced out in Austin, Texas are moving to more-affordable San Antonio or Killeen. For Denver, the affordability migration paths lead to nearby Greeley and Colorado Springs. Orlando households are moving to the neighboring Lakeland, Daytona and Ocala markets in search of better affordability.

The growth lanes are the next-ring affordability metros and exurbs. Re-ranking land toward value-commute corridors and tailoring plans to those buyers who are escaping high-cost hubs: provide efficient layouts, low maintenance living and strong schools.

2026 is a year to clear inventory, reprice land, lean into rentals and affordability-aligned geographies and pivot product to the demographics actually growing. Do that and stay nimble and you’ll be positioned for the stronger payoff period emerging in 2027 and beyond.

By Chris Porter. He is the Senior Vice President at Research John Burns Research and Consulting. He may be reached at cporter@jbrec.com.

By Chris Porter. He is the Senior Vice President at Research John Burns Research and Consulting. He may be reached at cporter@jbrec.com.

This column also appears in the January issue of Builder and Developer, read the print version here.