Navigating the New Home Market Strength

Builders must adapt to rising rates to put up a fight against affordability, practicality and tight inventory

By John Macke

By John Macke

The new home market has defied expectations in 2023, riding a wave of strength despite the challenges posed by 6%-7% mortgage rates. Large builders in particular have not only weathered these high rates but have thrived by adapting to meet affordability challenges and leveraging several key advantages.

Builders’ sales cooled month-over-month in August, as seasonally expected. However, the average sales rate per community is above typical seasonal norms. Strong gross margins have decelerated from record highs but still remain well above historical averages. And despite mortgage rates sitting at their highest level in 15 years, builders are ramping up production (starts) and are picking up their land and lot acquisition pace in response to continued demand.

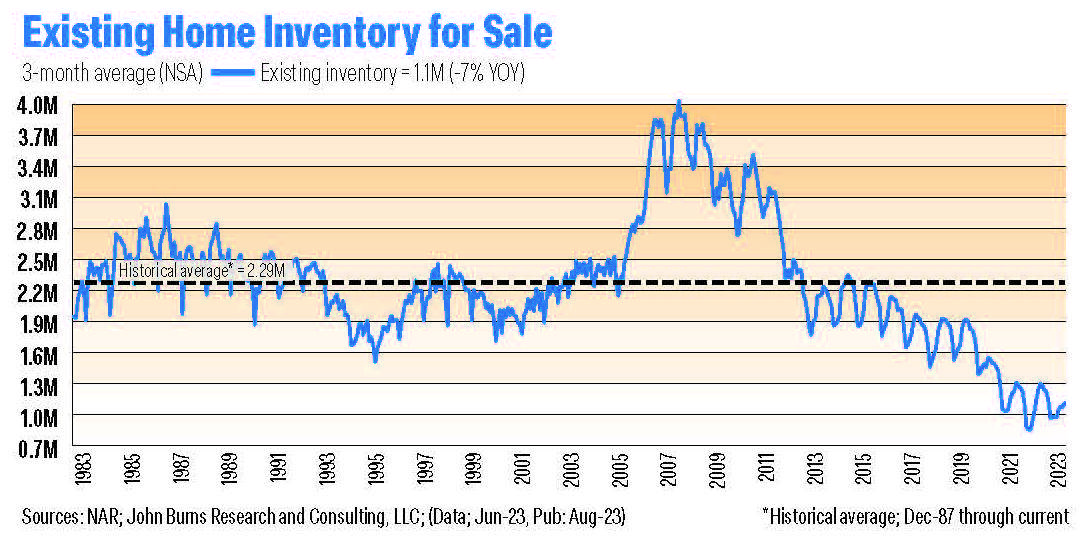

Tight inventory remains a key factor in the housing market, affecting both resale and new home markets. Resale listings are at an all-time low, hovering around one million nationwide, with no signs of a surge on the horizon, given homeowners are reluctant to trade their rock-bottom mortgage rates for today’s market rates.

The central challenge is the shortage of available for-sale housing supply. Buyers are often looking at the new home market given builders have available supply and the ability to offer below-market mortgages with rate buydowns or help with closing costs. The divergence in sales growth between existing home sales and new home sales is evident. Existing home sales closings have contracted by -19% YOY, while new home sales closings have surged by 24% YOY.

A big part of this divergence can be attributed to size and scale, plus key financial advantages thanks to: economies of scale that allow for operational and cost efficiencies as builders with market share may have the ability to work with trade partners and suppliers to reduce costs; limited reliance on regional banks, who have been tightening lending terms; and a much lower cost of capital, as larger builders can secure longer-duration financing at more favorable rates.

This financial flexibility affords more prominent builders a competitive edge in an environment where capital is vital for expansion and development.

As rates inch upward, builders are having a much harder time offering affordable products (especially for first-time homebuyers). In the first half of 2023, builders drove sales by buying down rates to the 4.75%–5.5% range. But as rates rise, there is concern regarding builders’ ability to buy rates down to acceptable levels for buyers without eating too drastically into the margin.

Our New Home Trends Institute team surveyed more than 1,300 homeowners and renters with household incomes of $50,000+ and learned that 5.5% is a critical threshold for mortgage rates.”

Our New Home Trends Institute team surveyed more than 1,300 homeowners and renters with household incomes of $50,000+ and learned that 5.5% is a critical threshold for mortgage rates. In this survey, 62% consider a historically normal mortgage rate to be below 5.5%, and 71% of prospective homebuyers planning to use a mortgage insist they will not accept a mortgage rate above this level. What happens when it becomes no longer financially feasible for builders to buy rates down below 5.5%?

To navigate these challenges, homebuilders must be adaptable. There are a few options outside of rate buydowns that homebuilders are using to manage affordability challenges: building smaller homes; and less customization and trimming down spec levels to more closely align with buyers’ essential needs.

Despite these affordability challenges, public builders have captured a significant portion of the market. In 2023, builders are fishing with a bigger net and a more enticing lure compared to the resale market. Strong gross margins give builders a buffer to offer financial incentives, namely competitive mortgage rates, while still remaining profitable. These rate buydowns have contributed to robust sales figures, even in a market where rates are 6% to 7%+. This approach has served them well throughout the year.

While we are still watching fundamental risks on the horizon, the ability to provide competitive mortgage rates and adapt to evolving market conditions remains critical for success.

John Macke is a senior research analyst at John Burns Research and Consulting.