The Pleasant 2023 Surprise

With new home sales and demand on the rise, what could unravel it?

By Brad Hunter

By Brad Hunter

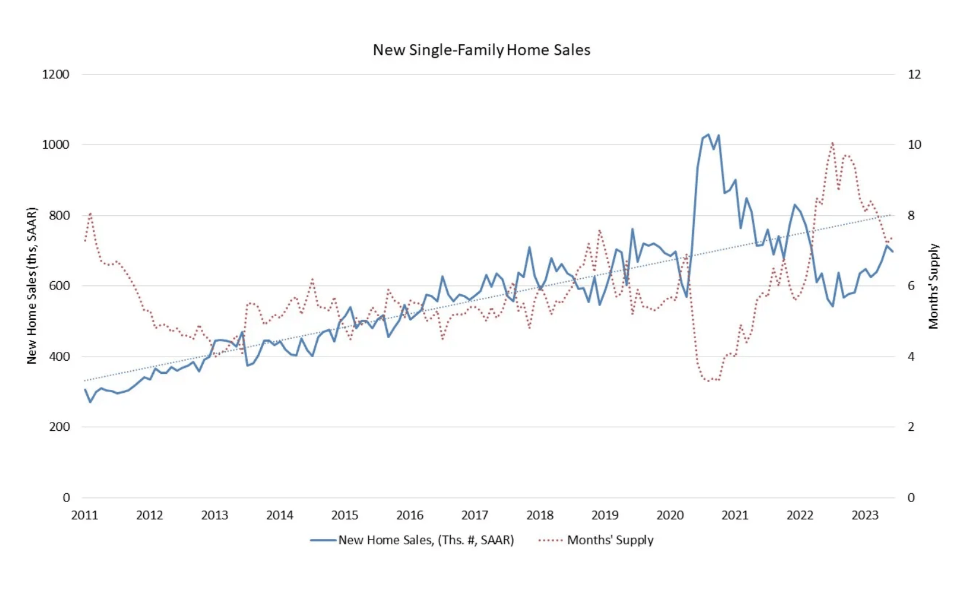

Every econometric model I’ve seen says that when you raise mortgage rates, housing demand goes decidedly downward. Sometimes housing demand gets downright clobbered. Yet, here we are with mortgage rates double what they were, and the housing market, following a short pause, is booming again (new home sales are up 23.8% versus one year ago, as of June)! And, homebuilders are tripping over themselves to buy more land for future residential developments.

The Fed wants people to feel a bit of pain right now. They want people to spend less on everything, and one of the levers they “know” they can throw to quickly slow the economy is the housing market. Just slowing down the purchasing of homes slows furniture and drapery sales, and all of the other hundreds of things people buy when they move. The Fed officials want more people to have trouble buying homes so that aggregate spending will slow down.

Yet, home sales are coming back up due to a combination of mortgage rate buydowns by builders, more households being formed by various age groups and a large number of people who are not affected by higher mortgage rates (read: cash buyers).

This raises two questions. Will demand for new homes eventually capitulate? And will mortgage rates go back down, or are they predestined by stubborn inflation to go higher?

What is Keeping New Home Demand So High?

Consumer confidence has been improving lately, and that is pulling up housing demand, from would-be homebuyers as well as prospective renters. Simultaneously, household formation rates, although slower than in 2021, are still quite strong (meaning, more people are moving out of shared arrangements and getting their own place). Demand is still “down” but coming back up at a rapid pace in the past 6 months. Consumer confidence has improved. The biggest risk here is that the long-predicted recession appears, which would drag confidence down, and demand with it.

But there is another important reason to consider, stemming from the lack of supply of homes for sale. Resale inventory got even tighter during the past year, which is in turn driving even more demand to the new home market. The number of homes listed for sale is half of what it would be normally because of the lock-in effect.

Builders are able to out-compete the existing home market, with their ability to buy down the mortgage rate, something that sellers on the resale market cannot match.

Even more important than that, builders have inventory, and that quick-move-in inventory represents head-to-head competition with the resale market. Remember, one of the reasons a homebuyer might prefer to buy a resale is that they can see it in person, and they can move in quickly. Right now, most builders can offer that same ability to prospective buyers. Plus, they can offer some personalization, and of course, a home that is brand-new, plus the aforementioned below-market mortgage rate, which is often the clincher.

What Could Go Wrong?

Low inventory and strong consumer confidence are the two lynchpins. It’s prudent to explore ways this situation could turn ugly. The chief risk to builders and developers (as well as land owners) is that the extremely low inventory of listed homes turns into a normal level of inventory (which would amount to a doubling of today’s inventory). What could precipitate that?

If the economic slowdown continues or intensifies, some homeowners (particularly owners of investment property) could come under additional distress and find themselves having to sell (foreclosures would also rise if a recession were to occur, which would further increase inventory). And, of course, that touches on the second lynchpin, consumer confidence, which always suffers in recessions.

The Take-Away

The key takeaway is that, so far, new home sales are holding up better than would normally be expected in the midst of a doubling of mortgage rates, but there could be a weaker patch ahead. We expect more builders to delve into the built-to-rent (“BTR”) segment in 2024/2025, which will take a bit of pressure off of the for-sale market.

Brad Hunter is president of Hunter Housing Economics, a consulting firm that provides site-specific market studies nationwide. He can be reached at brad@hunterhe.com.