A Look Ahead to 2023: Expect the Unexpected

Home values in 2023 may remain even stickier than in past downturns

By Patrick Duffy

A month ago, I wrote about three main inflection points in 2022 to consider for the economy and the housing market in 2023 and beyond, including inflation (and related mortgage rates), economic growth (or decline) and the extent to which remote work is here to stay. With the eventual fates of these points still up in the air, it shouldn’t be too surprising to see the variety of recent predictions on the housing market in the coming year ranging from the truly catastrophic to a soft landing.

However, before I get to that, I’d like to add three more trends which are likely to last far beyond the current business cycle which will add some additional mystery to 2023, including an ongoing supply/demand mismatch (especially for services), central banks turning off the money spigot and financial markets facing increasing turbulence. We’re now in a period of structural economic and financial changes around the world which will likely be accompanied by increased uncertainty, but that could actually be good for residential real estate as an asset class.

In a recent essay for Foreign Affairs magazine outlining these trends entitled “Not Just Another Recession,” economist Mohamed A. El-Erian also notes the dangers of central banks assuming that using the same financial tools which worked in the past will help us revert back to the days of 2019, but those days are gone because the world has changed. Previously the CEO of bond giant PIMCO, El-Erian is currently the President of Queens’ College at Cambridge University and advises Allianz, a global insurance and financial services firm.

Rising geopolitical tensions, more economic protectionism and building more resilient supply lines in the face of a changing climate will make it much harder to live in the world of two percent annual inflation to which the U.S. had become accustomed. Consequently, the challenge for the Fed now is to simultaneously reduce inflation as low as it can while minimizing disruption to growth and labor markets and also ensuring financial stability.

This might get messy in 2023 as the Fed and financial markets negotiate this new normal, as evidenced by the relatively high volatility in stock markets in recent months. In an article entitled “America’s Winners and Losers in Business” published by The Economist, over the last year the strength of tech-related companies reliant on bits, information and ideas has given way to stodgier ones which traffic more in physical capital and atoms.

Because so many tech-related companies are based in specific cities in California, Washington, Texas and Massachusetts, this shift in popularity back to old-economy companies could also have significant impacts on their associated housing markets, boosting the long-term fortunes of cities in North Carolina, Pennsylvania and New Jersey.

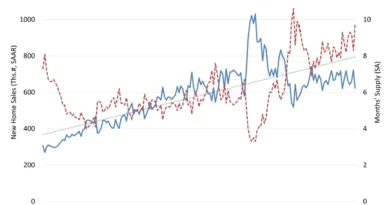

So what should we expect in 2023 for the housing market? If the financial crisis of 2007-09 is any guide, housing is somewhat unique in that it resists the rapid plunges in prices of other asset classes. While it is true that national home values did fall over 27 percent from peak to trough on the Case-Shiller Index, when they first began to fall in March of 2007, it took awhile for those declines to build momentum.

Over the next 12 months they fell less than eight percent year-on-year. It was during the following 12 months when those year-on-year values fell by nearly 13 percent as more sellers were forced to capitulate on price. During the additional three years through mid-2012, the annual decline in values steadily fell to the mid- to low-single digits as demand remained subdued. It really wasn’t until the middle of 2012 when home values again began to consistently rise — likely due to a combination of higher affordability and the share of investor sales consistently staying above 10 percent – that a new pricing floor was established.

There are also two key differences between now and then: The economy isn’t in a historic crisis, and more homeowners are taking a page from investors and choosing to rent out their homes instead of giving up hoped-for paper gains. As long as rents cover the payments for a mortgage with a low rate and other costs, home values may remain even stickier than in past downturns.

Patrick Duffy contributes as a Real Estate Economist for U.S. News & World Report and is the Founding Principal of MetroIntelligence.