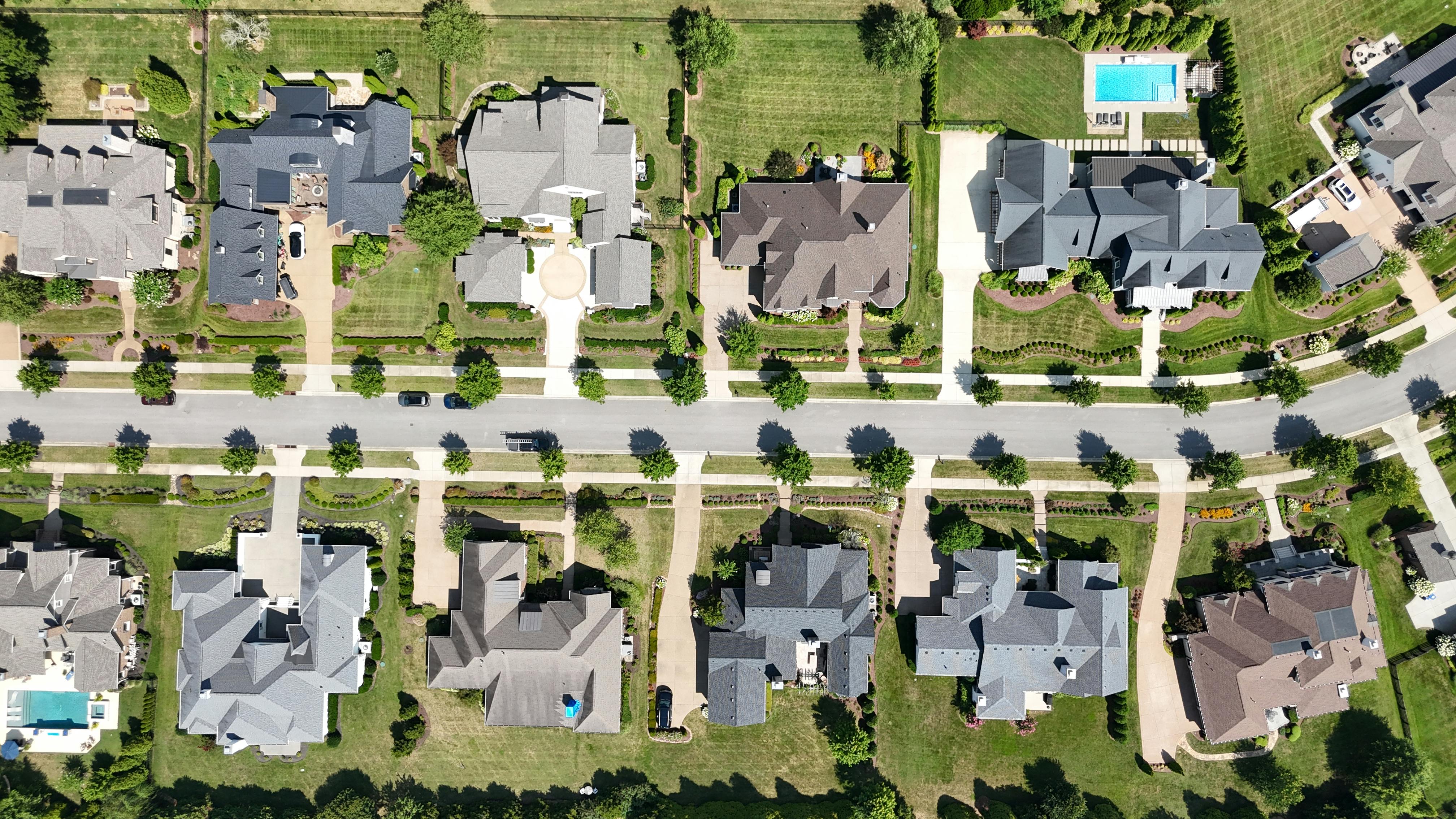

The Harvard Joint Center for Housing Studies released its annual State of the Nation’s Housing report, offering an overview of the current housing market. Many indicators show that housing market activity remained flat in early 2026. New home sales levels remained relatively unchanged, rental retention rates increased and new occupancies declined. Construction saw a slight decrease of 1% over the past year. Key takeaways from the report include subdued activity, weakening demand, and sidelined potential homebuyers.

The current weakness in housing demand is a direct result of several underlying economic drivers and a decreasing employment growth rate.

With many U.S. residents burdened by high housing costs, an increasing number of state and local governments are taking action to increase housing production.